Protect Yourself From Unnecessary Taxes & Market Downturns

Here’s serious advice for anyone with IRA or 401(k)s: Start getting your money out of these traditional accounts as soon as age 59 ½ if you can.

You might be wondering: “Why then, especially when it’s a time in life when many people are in their highest income and tax brackets of their lives?”

Because the notion that you’ll be in a lower tax bracket when you retire is more a myth than a reality for many Americans who are good about saving serious money for the future.

Stop Postponing Withdrawals

If you’re one of those with significant balances in your IRAs and 401(k)s, it’s easy to assume it’ll be better to wait to take withdrawals until your early 70s, when you have to start taking Required Minimum Distributions.

You might think, “I have plenty of money to live on from other income, investments, or savings, and the money in my traditional retirement accounts is tax-deferred, so all’s well, right?”

Well, actually, you’re just sitting on a tax time bomb.

Your traditional account balances will likely grow over time, which means you’ll be forced to withdraw larger chunks of money with your RMDs down the road. This can lead to bigger tax bills — especially if tax rates go up, which many people think they will.

And at the same time you’re paying taxes on those RMDs, you’re also likely paying up to 85% tax on your Social Security income.

And it doesn’t stop there. At age 65, your Medicare Part B kicks in, which could trigger IRMA surcharges (IRMA stands for Income Related Monthly Adjusted Amount). So if you’re also taking IRA or 401(k)s withdrawals after age 65, that can boost your income, which in turn could cause higher IRMA surcharges.

Essentially, with all of Uncle Sam’s taxes and IRMA surcharges, your money may not last as long as you think it will.

There’s a better way.

Save on Unnecessary Taxes With a Strategic Rollout

There’s a solution that can save you on taxes in the long run by putting your money in a position to be accessed tax-free during retirement. And it can protect your money from losses due to market volatility.

It’s called a strategic rollout. Not a rollover. A rollout.

With a strategic rollout, you transition money out of your IRAs and 401(k)s, getting taxes over and done with at current rates.

Then you reposition the money in a properly structured, maximum-funded Indexed Universal Life policy (what I call an IUL LASER Fund).

Why? Because IUL LASER Funds can provide:

Liquidity – Quick access to tax-free cash for just about anything you need — all without restrictions like an early withdrawal penalty before age 59 ½.

Safety – Protection from losses due to market downturns (with a 0% guaranteed floor).

Predictable Rates of Return – Rates historically averaging 5% to 10%, with any gains locked in upon each index strategy maturity date.

Tax Advantages – Tax-free growth, access to tax-free cash via policy loans, and an income-tax-free transfer of your death benefit/cash value upon your passing.

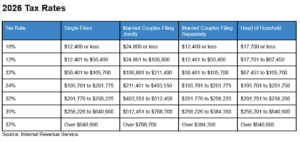

Use the Room in Your Tax Bracket

Source: Internal Revenue Service

One important strategy to consider when doing a strategic rollout is to take advantage of any room in your current tax bracket.

For example, let’s say you’re a married couple, both age 60, filing jointly with a taxable income of $105,000. You have over $500,000 in IRAs and 401(k)s you want to transition out of your traditional accounts with a strategic rollout.

In 2026, you would fall in the 22% tax bracket, which is for taxable incomes from $100,801 to $211,400. You start your strategic rollout by withdrawing $100,000 from your IRAs and 401(k)s, using that extra room in your 22% tax bracket. Then you put your after-tax withdrawal ($78,000) into your new IUL LASER Fund. (Note: This is based on 22% federal tax and 0% state. Keep in mind, state income tax can range from 0% to 13%.)

You repeat this process over the next four years, rolling the money out of your traditional accounts, getting taxes over with, and putting your after-tax withdrawals into your IUL.

By Year 5, you have put a total of nearly $400,000 to work in your IUL.

Your IUL Can Now Power Your Future

Once inside your IUL, you can benefit from indexing, where your money is linked to the market, while not actually in the market. Depending on index strategy performance, your cash value can grow tax-free — or be protected with a 0% floor if the market tanks. Historic average returns are typically 5% to 10%, but recently we’ve seen returns as high as 30% or more.

You can access money via policy loans absolutely tax-free for virtually anything, including retirement income, business ventures, education, emergency funds, etc.

You can choose to repay those loans or not — any unpaid loans are simply deducted from your death benefit/cash value upon your passing.

And you can give your heirs an income-tax-free transfer of your wealth with a death benefit that’s around $800,000 (could be more if your cash value has grown, or less if you have taken any policy loans that are still outstanding). This can be far better than having them inherit your taxable IRAs and 401(k)s.

In fact, non-spousal inherited IRAs and 401(k)s come with Uncle Sam strings attached. If you were already taking RMDs, your heirs typically have to continue taking those — and pay taxes on those withdrawals, which can push them into higher tax brackets.

And they typically have to empty your account within 10 years and pay taxes on the withdrawals (again risking going into a higher tax bracket), or face a 25% penalty.

Or they can have the peace of mind that comes with an income-tax-free death benefit that you pass on. (For more on avoiding the tax pitfalls of inherited IRAs and 401(k)s, read “What NOT To Do With That Inheritance.”)

For you — and your heirs — strategic rollouts make sense.

But don’t wait. Consider getting started as soon as you hit age 59 ½, when the 10% penalty for early withdrawals no longer applies. End your obligation to Uncle Sam as soon as you can, so you and your posterity can enjoy more of your hard-earned — and well-saved — wealth.

Action Steps: Conduct a Strategic Rollout to Protect Yourself From Unnecessary Taxes

Here’s how to guard against unnecessary taxes while protecting yourself from market downturns:

Educate Yourself. Dive into these concepts so you understand them fully — learn from charts, graphs, and real-life stories how IUL can protect your future by claiming your free copy of “The LASER Fund.” (You simply cover the shipping.)

Open Your Own Properly Structured, Max-Funded IUL. Work with a Certified IUL Professional to customize a policy that’s right for you.

Turn to Tax-Free Income During Retirement. Seize the opportunity to make your money last as long as you do by leveraging tax-free policy loans during your golden years.

Manage Your Wealth Throughout Retirement — and Beyond. Work closely with your IUL specialist to take advantage of safe arbitrage and indexing strategies during your retirement years — and leave an Equal Opportunity plan in place to pass along your wealth income-tax-free after you’re gone.

The Cost of Waiting: Why You Don’t Want to Procrastinate

Why give more of your money to Uncle Sam than necessary? His take on your retirement income could put you at risk of running out of money in your golden years.

Give yourself peace of mind by taking more control of your future.

Strategic rollouts can put you in a position to enjoy liquidity, safety, predictable rates of return, and tax advantages.

Get Started Today

Don’t miss out. Access our free books, attend our educational webinars, or connect with a Certified IUL Professional right here.

*Information in this article is for educational use only and does not predict or guarantee actual or future results.

________________________

Watch Doug Andrew explain these concepts in more detail on his YouTube channel…

Why Start Withdrawals at 59.5? Why is it smart to get money out of IAS and 401ks starting [music] at age 59 and a half? Recently, I had a YouTube viewer email me and ask, “Please tell me why I would start withdrawing from my retirement account at age 59 and a half when I’m still working and at the highest income and tax bracket of my life.” Okay. Well, I replied, “Most Americans uh who are savers, they save a lot in their retirement accounts and have a million to 2 million or more accumulated. They are not in lower tax brackets [music] when they retire, even though they have less income. And so, when people take money out of their 401ks, there’s six big mistakes that they make. Let me do a little bit deeper dive to answer this question. Uh why it’s smart to start getting money out at age 59 and a half. So, get ready. I think you’re going to be blown away with what I’m going to teach you in this episode. [music] So, I’m Doug Andrew. I’ve been a financial strategist and a retirement planning specialist now for north of five decades, helping thousands of Americans prepare for a comfortable retirement. And the vast majority of them when they come to me um at retirement, okay, at retirement planning something totally different than what you did for your retirement. And usually it’s optimal uh when they come in at least 5 years before they plan on retirement. Uh because we want to start a strategic roll out, okay? Not a rollover, a roll out. So, the six mistakes people make. Number one is Mistake 1 postponing taking money out beginning at age 59 and a half. Waiting around thinking why would I do that? Um, I’m at my highest income, my highest tax bracket that I’ve been in in my life. If you wait to take out money out of an IRA or 401k, uh, and you do it later, and most people who wait till later and take RMDs, that’s now if they have very much saved, they don’t realize that that they’re forced to pay tax on 85% of their social security. So that means every dollar that they take out of an IRA or 401k is not only taxed at 22%. [music] But it’s taxed at 22% on another 85% their social security. And so now every every IRA dollar is is being taxed uh you’re being taxed on on 185% of that IRA 401k dollar. Okay? Don’t do that. See what I’m doing by starting a roll out at age 59 and a half is I’m preparing people so that when they start social security uh that will not be hammered with taxes uh because the money coming out of an IL laser fund is taxfree. If if you’re getting IRA or 401k income out that forces people to pay tax on up to 85% of their social security. Now folks this this is big. And then, you know, some people worry about Irma uh that that’s the extra tax. If you make too much money, uh and you pull out too much money out of an IRA or 401k, that has to be, you know, two or three hundred grand. But but Irma is only an extra, you know, few hundred uh a month, uh $45,000 a year, which is minuscule compared to the amount of tax that we save by getting the the taxes over and done with and reposition into something tax-free. Okay, so that’s the that’s the fir first big mistake. Uh they postpone thinking they’re saving tax. People are in as high or higher tax brackets uh because they deferred and now they killed all their deductions even if they have a dramatically lower income. Okay. Now, second big reason or mistake is only taking out the minimum Mistake 2 needed. Okay. Well, I’m only going to take out what I need. thinking that you’re saving tax rather than taking advantage of all the room. What room? Uh before the next tax threshold now people say I don’t understand that. So let me go into this. For example, yeartoyear the thresholds increase a little bit. In 2026 for example uh a a single tax filer in a 22% bracket uh they they pay 22% federal tax on all taxable income. Taxable is after deductions and exemptions. Okay. Between 50,000 and 105,000 there’s 85 excuse me 55,299 of room. Uh [snorts] anything they they have in taxable income over 105,000 up to 200,000 is they have 96,000 of room. What am I talking about? Well, let’s say they made, you know, 150,000. A single person they make 150,000. Well, they they have another 50,000 of room to pull 50 grand out of an IRA or 401k and probably pay the lowest tax 22% that they’ll ever get away with because that 22 is going to go back up to 25. Okay? Uh and uh that’s not just 3% more. By the way, let me use a married couple filing a joint tax return. That’s a little bit more common in 2026. A married couple uh making uh a taxable income between 100,000 to 211,000. That’s $110,599 of room as shown here. Uh that uh you pay just 22%. Okay. Uh between 211,000 and $43,000 that’s 192,000 of room that you only pay 24%. That’s probably the lowest bracket you’ll ever be in. Why? Uh because you get rid of all these deductions and everything and you can get away with that. But hello, 24%’s going to jump up to 28%. Now, people say, “Well, that’s only 4% more.” Okay, no, it isn’t. If you have $1,000 of taxable income and you’re paying 24%, that’s $240, right? Okay. Now, if you pay $40 more than that at 28%. $40 is 16.66% more than 240. $280 is 16.66% [music] more. Uh it’s the biggest tax increase people will will ever realize in their entire lifetime if they wait around and let the uh tax taxes go up because the t the Trump tax [music] cuts passed clear back in 2017 were set to expire and then they got extended in the first year of Trump’s second term. But I’ll bet you sooner or later [music] uh it’s it’s going to expire and it’s going to go back up. Don’t wait around. Okay. [music] Now here’s the third big mistake. You’re repositioning those withdrawals. You take money out and you get the taxes over and done with. But then what do you do? You put it into a taxable investment. No, you don’t. I can’t believe how many CPAs and tax attorneys, they go, “Well, well, why would you tell your client to take money Mistake 3 out of an IRA or 401k?” I said, “To get the taxes over and done with these low rates.” They go, “Okay, but you’re just going to put it in something taxable.” I said, “No, I’m not.” Well, where you going to tell them to put it into something tax-free and also that will reimburse them at the end of the day when they finally die. So, their kids [music] uh they got reimbured for all the tax they paid. What’s that? Maxf funded IL insurance. You don’t save tax by stringing it out and deferring and then taking RMDs. That’s the worst advice for most Americans. But when you get the money out, you don’t put it into something taxable. You put it in something tax-free. I like a maxf funed IL because when I ultimately die, it reimburses my family for all the tax I paid because it blossoms when I die. Okay? If you don’t understand that, you need to understand IL. And I’ll show you what you ought to do to do that. I’m going to gift you a copy of my book at the end of this episode. [music] Now, the the fourth big uh mistake is not having a withdrawal strategy based on your optimal tax bracket. Things change. And so that’s why I always have met with my clients uh annually uh before the end of the tax year to determine how much we want to get the the taxes over and done. How much room are we going to have this year? And even if I went slightly over uh you don’t pay retroactive a a higher tax rate back to dollar one. You only pay the higher tax rate on on maybe the thousand that you went over. I’d rather I’d rather go a little bit over than a little bit under. I want to take advantage of of the current tax bracket at today’s lower rates while account values are lower. Okay. Uh the fifth mistake is when people are duped into taking RMD uh yeah the required minimum The RMD, 4% Rule, and Heir Problem distributions RMDs. Okay. I can’t believe how many people are told well if you don’t need the money just take just take the required minimum starting you know at age 73 74 depending upon your situation. And then also using the pathetic 4% rule where the financial services industry recommends you only take out 4% so you will not run out of money. Uh that’s ridiculous. That’s unacceptable to me. And I’ll I’ll illustrate that in just a moment. Uh the last uh one is is leaving behind 401ks and IAS to non-spousal. Uh once I teach this to CPAs and tax attorneys, they just go, “Oh golly, you’re right.” um they agree the worst place to leave money uh to your heirs is in a yet to be taxed IRA or 401k. Well, basic reason is they can’t wait until their retirement uh and then pay tax. They have to pay tax on that within 10 years of inheriting your IRA or 401k whether they’re retired or not. It’s stupid. You need to get the taxes over and done with sooner or later. Okay, those are the mistakes. Now, let’s get back here. Let’s uh use an example of IRA or 401ks um in the market using the 4% rule. Uh if you had a million and $250,000 in a nest egg using the financial services industry standard of don’t take out more than 4% a year so you won’t outlive your money. Uh that’s only 50,000 bucks. [music] Okay, that’s pretty pathetic. I don’t accumulate a million 250 grand to have a measly 50,000 a year of income. That’s what the financial services industry recommends. Uh that’s before tax. In a 28% bracket between federal and state, uh again, 41 out of 50 states out of state tax. Uh so 28% would be 14,000 in tax. You’re only netting 36,000 to buy gas, groceries, prescriptions, or golf grain fees. Not only that, but you could very possibly uh be uh be be being paying tax on 85% of your social security if this is on top of other income. That’s stupid. Okay. Now, an IL with a,250,000 in it can give you an 8% payout to age 120. That’s 100,000 a year. It’s not a little bit more, it’s a whole lot more. Okay? uh at a 10% payout, which is what most our clients uh are able to realize, that’s 125,000. Okay? [music] Uh why why generate 36,000 when you could generate 100,000 or more? Uh it’s triple. Okay? Now, let me show you an actual example here. Um we had a fellow come to us at age uh 70 and a half back when that was when RMDs were required. This was in 2012. And he had 600,000 in his IAS. The sad thing is he had 600,000 in his IAS 12 years earlier in the year 2000. Now he didn’t add any more money but that 600,000 in 2001 to 2003 dropped down to 6 360,000 in the market [music] and it took until 2007 to come back to 600. [music] he lost uh 40% again. It went down to 360,000 in in 2008. It took Real Client Example four more years to come back to 600,000. So 12 years and he was barely back to where he was 12 years earlier. And his advisor who came to the office uh with him [music] uh said, “See, I told you the market always comes back.” Yeah. Hello. That was pathetic. Especially when he learned that our clients tripled their money. He could have he could have had a million8 in an IL if he would have been in an IL instead of in the market being linked to the S&P but you know we were dealing with what he had. Uh and then his advisor did what? Recommended he takes only 4% a year. Yeah. That’s that’s a measly 24,000. Uh that’s before tax. He was in a 33% bracket. He was only netting 16,000 or you know 1333 bucks a month. How pathetic is that? Uh we did a strategic roll out and uh we uh uh we were able to reposition the 600,000 and and manage that and and give him an average of 8 and a quarter% uh over the five years that we got it out of his IRA. Uh so we were able to pull out 150 grand a year. Now worst case in a 33% bracket, he’s paying 50,000 in tax every year uh for five years on that. He’s only netting 100,000 to go into the IL. If that’s all we did, at the end of 5 years, he’s got 500 grand in the IL. He can pull out 10% a year the rest of his life, which is 50 grand. How much more is 50,000 than 16 triple? We do this all the time. Okay. Uh but uh if he dies with the IL with the if he dies with the IL, he leaves behind a million tax-free. Now folks um in actuality what we did is we got all 750,000 out taxree. The 150,000 a year he got out taxfree. How did we do that? I’m a tax strategist. Uh The 3-Step Strategic Rollout I resurrected deductions that he’d been killing on some of his rental property. I’ll show you what I’m talking about here in just a second as I wrap up. Okay. What is this three-step process? It’s a strategic roll out. We strategically reposition re retirement funds, subjecting them to tax, taking care of taxes now rather than postponing and increasing the inevitable liability and also avoiding having to pay, you know, uh uh tax on your social security, 85% of your social security. Uh number two, uh we reposition the net after tax into something tax-free from now on and it will eventually reimburse you when you die out of an IL. So you’re not out anything. uh but you’re you’re now switching to tax-free. And then number three, we don’t always do, but that’s where you offset some or all of the tax by resurrecting deductions they had been killing. So, this fellow had some uh rental properties that had been killing the tax deduction by taking his his rental income and and paying against the mortgages, thinking, “Oh, uh that’s the best thing to do is just pay down the mortgages.” And no, he realized that was sort of stupid. So, he refinanced four of his duplexes for a million dollars each. Every one of the four duplexes, he took out a million-doll loan at 7.5% interest. Now, he did it at 4 and a.5%. Uh, but even at 7.5%, that’s 75,000. That’s a new deduction, okay, that you didn’t have. That allows you to realize 75,000 of income or 75,000 you could pull out of an IRA or 401k with no tax. Now, he did back when he we did this in 2012, it was 4 and a.5% interest. And in his tax bracket, that was a net cost of of three. Here, if you borrowed at 72, that’s a net cost of five. The reason why I’m doing this, even though he he borrowed at four and a half, is interest rates are relative. I’m I’m showing you even at higher interest rates. Uh you you borrow at 7 and a half in a 33% bracket, it’s a net cost of five. It’s it’s a net cost of and he’s making 10. That’s 100. How much more is 150? That that that’s 100% more. [music] He was actually making 300% more. He was he was paying 30,000 on his mortgages and uh making on his IL 90,000. Would you hire an employee for 30 grand that made you an extra 90 grand? I’ll do that all day long. But even conservatively here, uh you will make 100% more than the cost of the mortgage, even if it’s vacant. If it’s paid off or you’re sending extra principal payments to the mortgage company and it’s vacant, you don’t you’re you’re you’re you’re trapped. So, if you want to uh learn how to do this or read stories, I have several stories Next Step in the right brain side of this book, but you can understand why it’s taxfree under the left brain side of the book. Uh this has been flying off of our warehouse shelves. Uh the laser fund, how to diversify and create the foundation for a taxfree retirement. And uh it retails on Amazon for anywhere from 20 bucks up to 60 bucks plus shipping. If you buy it on Amazon, thank you, but I’ll gift you a copy for free. Uh simply go to laserfund.com or click on the link below and you contribute a nominal amount toward the shipping and handling. I require a little skin [music] in the game uh and I’ll pay for the book. I’ll fire out a hard copy to you via priority mail. Now, uh, when you’re in there claiming your free copy, uh, if you like to watch and learn or listen and learn, there’s [music] those formats available for a nominal investment, too. You can also schedule to attend one of our educational webinars that we do every week. No cost, no obligation. You can even schedule an appointment to talk to an IL professional that I oversee uh that that are certified because it’s imperative uh that you see how a property structure max funded ILER fund works with your numbers. uh you over 90% of ILS are not structured correctly and I don’t want you to make that mistake. So you want to uh make sure somebody who knows what they’re doing structures it correctly. Okay? And so uh this book is two books in one. The the left brain side is the is is the white covered side about 200 pages. The right brain side that contains 62 actual stories is is the right brain side. If you want to use your whole brain, uh, read both of these books. But, uh, this is going to make a transformation in your future and you’ll understand why it’s smart to get money out of those IAS or 401ks sooner than later at age 59 and a half. Uh, don’t postpone. Uh, don’t trigger tax on 85% of your social security. Uh it it’s much more complex than just well why would I do that when I’m at my highest income and highest tax? You this this is not going to be uh your the your current tax bracket is likely the lowest bracket you will ever be in even if you have less income is my message here. Okay, don’t make that mistake and I’ll see you on the other side of your brighter future.

________________________

Frequently Asked Questions

How do I perform a strategic rollout? Connect with a Certified IUL Professional who can walk you through repositioning your money, efficiently getting your taxes over with, and properly structuring and maximum-funding your policy.

Is there any risk of losing money due to market volatility in a LASER Fund? The IUL LASER Fund strategy is built for safety—your principal is protected from market losses and credited interest can only go positive or zero, depending on market performance.

What makes an IUL “properly structured” or “max-funded”? A properly structured, max-funded IUL LASER Fund is optimized to minimize costs and maximize potential cash growth, staying within IRS guidelines to preserve tax advantages.

Where can I learn more about the IUL LASER Fund or start my own policy? Order our comprehensive “The LASER Fund” book for free (you just cover shipping) at laserfund.com, attend a virtual educational event, or connect with a certified expert by clicking here.

Still have questions? Want to unlock your own tax-free retirement plan?

Connect with an IUL LASER Fund specialist today: Get started now.