Where do you put money, the kind of serious cash you want to save for retirement?

Pay attention to what the wealthy do: Wealthy people don’t use banks to park money that’s earmarked for long-term goals. They know that giving your serious cash to the bank is one of the worst ways to save, because the bank just uses your money to get rich themselves.

What do the wealthy families in America do instead? Many of them want their money to go further. They also want more tax advantages. So they open several properly structured, maximum-funded Indexed Universal Life policies (what we also call IUL LASER Funds).

Why? Because when compared to traditional bank and credit union savings accounts, CDs, and money markets, IUL can be a superior capital accumulation tool, with historic average interest rates that typically outperform traditional accounts.

Taxes – IUL vs. Traditional Accounts

The wealthy also understand that IUL’s advantages go further than many traditional accounts, including IRAs and 401(k)s, particularly when it comes to taxes.

Tax-Free vs. Taxable Growth – Interest earned in an IUL policy is typically tax-free. Your earnings in most bank or credit union accounts are taxed as ordinary income each year. And while tax-deferred, when you withdraw money from IRAs and 401(k)s, Uncle Sam takes his share on any growth.

Tax-Free vs. Taxable Access – When you access money with your IUL via policy loans, that income is absolutely tax-free. When you withdraw money from your IRAs and 401(k)s, you’ll pay taxes every time.

Income-Tax-Free vs. Taxable Transfer – When you pass on, your IUL death benefit transfers income-tax-free to your heirs. When your heirs inherit your IRA or 401(k), they will be taxed on withdrawals they make — and if they don’t empty the account within 10 years, they’ll also face a 25% penalty.

Penalty-Free vs. Penalties – IULs don’t have age minimums or Required Minimum Distributions — you can access money at any age or leave the money in the policy until you pass on; it’s up to you. With your IRAs and 401(k)s, on the other hand, you’re typically hit with a 10% penalty for withdrawals before age 59 ½. And after a certain age (currently age 73), you have to make Required Minimum Distributions or face penalties.

The Three Tax Codes Behind IUL’s Advantages

There are three Internal Revenue Codes that help IUL stand out from other financial vehicles:

Section 72(e) – This section dictates that money that accumulates inside of an insurance policy typically does so tax-free.

Section 7702 – This section defines the three types of income that are taxable: earned, passive, portfolio. Because insurance loans don’t fall under any of those categories, the money you access via policy loans is tax-free.

Section 101(a) – This section makes it possible for your money to transfer income-tax-free to your beneficiaries as a death benefit.

How Does IUL Work?

Now let’s look at an illustration to understand more of how IUL works.

In this scenario, let’s say you have $500,000 you want to set aside in an IUL policy.

To make it an effective cash accumulation vehicle, you want to put in the most allowable, with the least amount of insurance under IRS guidelines.

So you open a policy with a premium bucket big enough to accommodate $500,000, which will provide about $1,000,000 in minimum life insurance.

To comply with IRS guidelines, over the next five years, you fill up your premium bucket in five equal annual payments of $100,000 each.

There are annual costs to your insurance, which include the pure cost of the life insurance, or the term component inside the insurance policy, and any other fees associated with managing the policy. In this illustration, the cost of the insurance is represented by the spigot on the bottom right of the bucket.

Now before you see that “cost flow” as a negative, consider this. The little stream of water is actually going to work for you. It’s what’s paying for your policy, which in the end will provide a valuable death benefit to your loved ones. It’s essentially “watering” a nice little money tree that will blossom and transfer whatever was left in the bucket to your heirs or beneficiaries, income-tax-free, upon your death.

When you open an insurance policy, you want this spigot to drain out the least amount of costs as possible so that your internal rate of return will be the highest possible. The average annual return that most people have achieved during the last nearly thirty years is 5% to 10% (with some even experiencing higher average returns). This spigot has drained out an average of about 1% over the life of the policy, thus netting an average of about 4% to 9% interest compounded annually on a tax-deferred basis (and being able to access it tax-free for income).

As you max-fund the insurance contract and it grows tax-free, over time your cash value can eventually equal the death benefit, often by about Year 11 to Year 15. When that happens, you’re essentially assuming 100% of the risk — you’re self-insuring — which brings the cost of insurance down.

Let’s say you have $1 million in the policy that’s earning a historic average of 5% to 10% (our clients often average more). You can typically safely access $50,000 to $100,000 a year in retirement, without depleting your principal.

You can use this income for anything, not just retirement. Many wealthy people turn to their IUL LASER Fund to act as their own banker, borrowing money via policy loans for things like real estate ventures or working capital. They’ll repay the loan then turn around and borrow again for the next initiative, and so on. (Note that policy loans don’t require repayment. Any unpaid loans are simply deducted from the cash value/death benefit upon your passing.)

Now there’s another advantage of IUL over traditional retirement accounts: the opportunity to take advantage of market upturns, while being protected from market downturns.

With IUL, you can link your money to different index strategies, without your money actually being in the market. When the market goes up, so does your cash value. When the market drops, you’re protected with a 0% guaranteed floor.

Real-Life Example of Growth Potential

Let’s look at a real-life client experience to understand these concepts better.

In March of 2020, the market dropped 30% in one single month due to COVID-19.

At that time, we contacted hundreds of our clients and said, “This is unique. The market’s down 30%. The chance that it’s going to be higher than that a year from now is highly likely. We would recommend you link some or all of your money in your insurance policy to a one-year point-to-point with no cap, with a 5% threshold.”

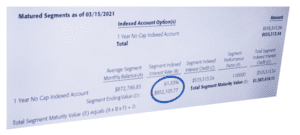

Sure enough a year later, in March of 2021, the market went up 66.33%. After the 5% threshold, our clients with this uncapped strategy netted 61.33%.

One particular client had allocated $852,000 to this index strategy, and he made $535,000 tax-free in one single year.

Now, this isn’t to say that’s typical — as mentioned, IUL has historic average returns of 5% to 10%. But by diversifying index strategies, it’s possible to earn significant returns. And when the market tanks? Remember, you’re protected from losses due to downturns with that 0% guaranteed floor.

These are the kinds of strategies wealthy people use.

This is why they don’t keep their money in a bank or credit union, because they don’t want to miss out on the advantages of IUL.

Action Steps: How to Take Advantage of Tax-Free Growth and Tax-Free Access

Assess Your Current Plan: Identify where you’re putting your serious cash and consider the level of liquidity and tax advantages you currently have.

Learn More About IUL: Learn about the significant advantages of a properly structured, max-funded IUL (what we call an IUL LASER Fund). Order a free copy of “The LASER Fund” book at laserfund.com (you just contribute to shipping and handling).

Connect With a Certified IUL Professional: IUL is complex and requires proper structure and funding for optimal growth potential. Be sure to work with professionals who are certified, so your policy can be optimized for growth, flexibility, and tax-free access.→ Find a certified agent now

Attend a Workshop or Event: Reserve your spot in upcoming educational events to deepen your understanding and take advantage of market cycles.→ Upcoming Events

First step to take today: Start with a no-obligation review of your current retirement strategies and see how a tax-free IUL LASER Fund can impact your financial future. The boost may surprise you.

Avoid Missed Opportunities

If you rely solely on traditional savings or retirement accounts, Uncle Sam will likely enjoy a larger share of your money than necessary.

What Could Happen If You Don’t Take Action?

You might outlive your money due to taxes and market losses.

Your beneficiaries will likely inherit less—potentially much less.

You forfeit the combined power of tax-free growth and access to tax-free cash.

Why the wealthy don’t bank like you. Why do wealthy people never use banks to park their money that’s earmarked for long-term goals? Because the bank is using your money to get rich themselves. Okay? Wealthy people become their own banker. Parking your cash in a bank is actually a wealth leak. giving up safety, rate of return, and with most bank accounts, uh, taxes punish you. It’s the worst way to save, and I can prove that to you. So, what do the wealthy families in America do instead? They build what I call a 3 Dimensional family bank. And for the financial dimension of the three dimensions, they create several properly designed max-funded cash value insurance contracts or policies that keep money liquid protected and create tax-free access, tax-free income as well as tax-free transfer. So, I’m Doug Andrew. I’ve been a financial strategist and a retirement planning specialist for now north of five decades, helping thousands of Americans optimize their assets and minimize taxes and uh help them become their own banker. Now up here on the screen I have three sections of the internal revenue code. I teach these three sections of the internal revenue code to CPAs and tax attorneys uh in advanced continuum education. And so they come to learn about these sometimes after they’ve been in practice for years and they always do this. Oh my heck. I I didn’t realize how powerful uh these three sections of the code are. Now what do they have to do with my favorite financial vehicle? if you’ve watched very many episodes on this channel is a properly structured max-funded IUL. And Three Tax Rules if it’s properly structured and it’s funded uh to the max usually within 5 years, it turns into a tax-free capital accumulation tool to accumulate money. Okay. Now, how does it do that tax-free? Well, under section 72E of the Internal Revenue Code, uh, money that accumulates inside of an insurance contract, a life insurance policy will always grow, uh, with interest, dividends, or whatever, tax-free. Now, most people use life insurance for death for death benefit. EF Hutton said, uh, why don’t we use this tax-free accumulation for living benefits instead of just the tax-free death benefit? Well, 72E says the money that grows inside those is tax-free. So instead of trying to get X amount of life insurance for the least premium to pay off when you ultimately die, all EF Hutton said is why don’t we do the opposite? Why don’t we pay the most money into this insurance policy that the IRS allows? use it for tax-free growth and tax-free income where we can earn a gross rate of return if it’s managed well uh of uh 10 11 12% and yeah I’ve been able to earn uh 11.17% uh gross rate of return in the worst 10-year period since the great depression 2000 to 2012 that is afforded under how you structure the IL index universal life correctly and the money accumulates is tax-free under section 72E. So section 72E has been around in the Internal Revenue Code for in one form or another for about 120 years as of the recording of this episode. And so EF Hutton said why don’t we utilize that? Now this section 7702 dictates how you can access money uh out of that insurance contract uh without paying tax or 10% penalties. is you don’t have to wait till you’re 59 and a half. Uh you have money in there. It it dictates how you access it the smart way so that you don’t trigger tax or penalties or anything like that. And then section 101A is really the magic. It’s where you are self-insuring. You’re taking your money and putting it into the insurance contract and you are going to own the death benefit uh instead of uh uh pay for it. So that all of a sudden your Tax-Free Access money over time actually is tax-free because you assume 100% of the risk as your money grows to equal the death benefit. Okay? It’s it’s really that simple. But it’s amazing how many uh financial advisors never learn this. So accumulate your money tax-free, access your money tax-free when you die. It it blossoms. It increases in value and transfers tax-free. Nothing else does that in the internal revenue code. I’ve asked CPAs and tax attorneys for years. show me any other financial instrument in America that does that and they they’ve yet to show me. I’m going to use a very simple example cuz uh a whole lot of high net-worth people and this video is about why wealthy don’t bank like you. What what do they do? They use this and so uh they are repositioning all kinds of assets from their real estate portfolios and and all their bonds and stocks and mutual funds and everything like that. I’m going to keep this really simple. I’m not going to even act like you’ve been earning interest on this, which you would have been earning when you have 500,000 in there because your cash uh should be equal the premiums you put in even with all the cost that’s spitting on the bucket, which is the cost of this insurance that has to be there in order for it to be tax-free. Okay. But if I have 500,000 in there, yes, there is an option called an increasing death benefit that if I died, then this would be paid out on top of that uh uh and a,ion500,000 would be paid out uh when I die. But that’s not the objective. I told you uh people want the best internal rate of return. And so that’s that is option uh usually a which is the level death benefit. That’s where you want any money that’s accumulating in here to be qualified as part of the death benefit. So, you’re self-insuring. So, when you have 500,000 of cash in there and uh you die, they only pay out a million still, but they were only charging you when you put in 500,000. By the time you got that in there, they’re only charging you for the net amount of risk. So, if if 500,000 of that million is your own money, they’re only charging you down here. pick it on the bucket now is half the size it was 3 years ago 3 years earlier 3 years in one day. So the net amount of risk is only the remaining 500,000. So you’re only paying for half as much life insurance as you were 3 years ago. Uh assuming you’ve done this IUL Cash Growth for 3 years in one day. Now most of mine have been averaging uh net 9.62%. Uh that’s after all cost and everything like that. 9.6 6 divided into the rule of 72 means uh your money doubles every 7 and 12 years. So many of our clients when they get 500,000 in there that will double to be worth a million uh in by the 10th year 10th and 11th year by the 15th year whenever but let’s just use that as an example. So in 10 and a half 11 years into this IL now your cash equals the death benefit. Now, you tell this to most um whole life insurance agents and they they don’t even understand how you did that. Well, that’s because whole life can’t do this. You’re you’re you’re actually owning the death benefit. You are self-insured. Truth be known. If I died when I have a million of cash in there, the insurance company pays out 5% more than that. They pay out a million50,000. Uh that is what has to happen uh until you’re age 95. They pay out 5% more uh in order to be a tax-free insurance contract under TEFRA uh but they’re only charging you for 50,000 net amount of risk. Okay. 120th the uh the death benefit you were paying for 10 years earlier when you started. Okay. And the cost of of 50,000 uh is dwarfed by the interest you’re earning on a million. And that’s why uh if you want to start taking out income, you can start pulling out 10% a year, 100 grand a year out of that million without depleting principle because we show you how to diversify with indexing and rebalance. And you can earn uh if you do that, you know, 11, 12, 13, 14. If you earn 11, you’ll net 10 uh retroactive back to day one because only 1% of your interest was actually covering the cost of the insurance that the IRS had had to be there. in order for it to be tax-free. If you don’t need income yet, you let it sit there for another 7 and a half years and uh the million grows to 2 million. If you happen to die, then they’ll pay out 2.1 million, but they’re only charging you for 100,000 of net amount at risk. The interest you’re earning on 2 million bucks dwarfs the cost of life insurance uh of a 100,000 even though you’re 17 years older. See, the insurance is getting cheaper and cheaper as you get older to where you go down the road 20 and 30 years. You wouldn’t believe how many people look at the internal rate of return and if they earned 11 and they’re netting uh usually around 10.85 uh in that given year, it’s incredible. But retroactive back to day one, we usually say, well, if you earn 11, uh you’re going to net 10 retroactive back to day one. And this is how the insurance gets cheaper as you get older. And so when you have annual reviews like March of 2020, uh what happened? COVID. Market Opportunity Example Now the market dropped 30% in one single month. Uh when there’s anxiety, that spells opportunity. And we contacted 800 IUL clients and we said, “Oh, uh this is unique. The market’s down 30%. The chance that it’s going to be higher than that a year from now is highly likely. uh we would recommend you link some or all of your money in your insurance policy to a one-year point-to-point with no cap. Now, people say, “Well, why why wouldn’t you choose a no cap all the time?” Because uh there’s a cost to that. It’s a threshold strategy. Uh if the market went up 12, they subtract five percentage points. So, if you earn 12, you’re only netting seven. And, you know, like I said, we we usually average around, you know, 11 or 12. And so we don’t want to earn 12 and only net seven. Uh we can we know we can earn 12 and net 11 or earn 11 and net 10 uh by managing the way the economy normally is going. But when there’s anxiety, there’s opportunity. So there was going to be 5% subtracted. That’s okay. In March of 2021, the market was up 66.33%. Minus 5% and they netted 61.33%. This client had allocated $852,000 in his IUL to a one-year point-to-point with no cap. He got credited 61.33%. Uh at the end of one year, March of 2021, it was worth a,387,000. He made 535,000 tax-free in one single year. Now, those come few and far between. But when you seize those opportunities, uh that’s what offsets the zero years. And uh usually only about 30% of the years do you get zero but you don’t lose. And that’s what takes your average return from you know 7 8 or 9% up to 11 12 13 14% when you can always seize those opportunities. That’s what the wealthy people do. That’s why they don’t keep their money in a bank or credit union because they’re missing out on liquidity, safety, rate of return, and tax-free benefits. Well, folks, uh hopefully you’ve gained some insights here. I would implore you to search other episodes on why uh the wealthy uh do not use uh typical banks, but you can learn this in my most recent bestselling book, The Laser Fund. This is actually two books in one. This white covered side is about 200 pages, 14 chapters with all the charts and graphs and explanations. If you’re a left-brain learner, if you’re more of a right-brain learner, you learn more by stories. uh you can just flip it over to this orange one which is about 100 pages, 12 chapters with 62 actual client stories. And if you want to use your right brain and your left brain, then you can uh use your whole brain and read the entire book. Uh but uh you can buy this on Amazon for 20 bucks up to 60 bucks. I’m not trying to sell you my book. I’ll gift you a copy. Simply go to laserfund.com or click on the link below and you contribute a nominal amount towards the shipping and handling. I require a little skin in the game. uh I will cover the rest of the shipping and handling costs and I’ll pay for the book. I will fire out a hard copy to you via priority mail. Okay? Now, while you’re in there claiming your free copy, if you also like to listen and learn and watch and learn, there’s always formats available for a nominal investment. And uh you can even schedule an appointment to talk to an IL professional that I train and oversee and they will actually show you how a properly structure max benefited IUL will work in your particular set of circumstances to optimize under-performing and non-performing assets where you currently have money and you want to increase liquidity, safety, rate of return, and tax benefits by exploring what if you were to put that money into a properly structured IUL. You’re going to be blown away with how much better off you can be.

Frequently Asked Questions (FAQ)

1. What is an IUL LASER Fund, and how can I use it in retirement planning?

An IUL LASER Fund is a properly structured, max-funded Indexed Universal Life (IUL) insurance policy designed to maximize tax-free growth, provide flexible tax-free access to cash value, and deliver an income-tax-free legacy to beneficiaries.

2. How does tax-free retirement income work with an IUL?

You can access your IUL LASER Fund’s cash value through policy loans, which are not considered taxable income. This strategy enables you to access income before and during retirement without triggering taxes or penalties—unlike traditional IRA or 401(k) withdrawals.

3. What are the main benefits of a max-funded IUL vs. a Roth IRA?

A max-funded IUL offers six major benefits, including no contribution limits, no income-based restrictions, tax-free compounding, no 10% penalty for early withdrawals, and an income-tax-free death benefit. Roth IRAs deliver only two of those six advantages and limit your annual contributions.

4. Is Indexed Universal Life insurance safe for retirement income?

When structured and managed correctly, an IUL offers downside protection because your cash value is linked to—not invested in—the market. Your principal is shielded from market losses with a 0% floor, making it a safer vehicle for predictable, tax-free growth.

5. How do Indexed Universal Life insurance policies perform in volatile markets?

IUL LASER Funds can excel during volatile markets because they capture gains in up years but do not suffer losses due to market volatility in down years. Real-world statements show double-digit tax-free returns even during turbulent periods, as seen in 2020–2021.

6. What is the role of a certified IUL agent?

Certified IUL agents have undergone advanced, rigorous training to design IUL correctly, ensuring you can maximize all six advantages and avoid costly mistakes like failed IUL design that can lead to added cost and policy under-performance.

7. Can high net worth individuals benefit from max-funded IULs?

Absolutely. Unlike Roth IRAs, LASER Funds have no income or contribution limits and are especially suited for high-net-worth individuals seeking predictable, safe, tax-free accumulation and legacy planning.

8. Where can I see real IUL policy performance statements?

You can review dozens of verified annual policy statements posted to the IUL Performance Watch website. These provide monthly, up-to-date proof of actual client results.

9. How do I start an IUL LASER Fund for tax-free retirement income?

Begin by connecting with a certified IUL professional, request a custom performance review, and compare your current retirement approach to the LASER Fund strategy. Click here to get started.

Still have questions? Want to unlock your own tax-free retirement plan?

Connect with an IUL LASER Fund specialist today: Get started now.