Don’t Let Uncle Sam Win

If you have recently received (or are soon to receive) an inheritance of an IRA or retirement account…heads up. Uncle Sam has plans for a good chunk of that money coming your way.

If you have recently received (or are soon to receive) an inheritance of an IRA or retirement account…heads up. Uncle Sam has plans for a good chunk of that money coming your way.

With the SECURE Act of 2019, rules went into play for IRAs and retirement accounts inherited from 2020 on.

In most cases, you have just 10 years to withdraw the entire balance, or face a 25% penalty on what’s left in the account (called the shortfall).

That’s not all: In addition to making sure you empty out the account within 10 years, if the deceased was old enough to be taking required minimum distributions (RMDs), you’ll typically need to continue those RMDs, regardless of your age.

Uncle Sam Wants More of Your Inheritance

Now why do you think the government is giving you a 10-year deadline to bottom out that inherited account?

IRAs and traditional retirement accounts are tax-deferred — meaning you’ll pay taxes when you withdraw the money. And Uncle Sam is clearly going to be patient for only so long until he gets his due.

Still, you might be thinking, “Hey, 10 years is pretty long, maybe this whole mandatory withdrawal deal isn’t so bad,” until you consider the potential impact of the taxes you’ll pay on those withdrawals.

Withdrawals from inherited accounts can push you into a higher tax bracket, which means more for Uncle Sam and less for you.

What’s worse, if you don’t need to access the money, you might be tempted to wait until the last year or so to empty the account. Now imagine how much further that lump sum could push you into even higher tax brackets.

All of this gets even more unsavory when you consider whether taxes are likely to go up or down in the future. If you’re like most Americans who believe they’re only going to increase, it doesn’t help to procrastinate your inherited account withdrawals.

Sorry, Uncle Sam

So don’t wait. Get smart about that money right away and consider a strategic rollout.

We’re not talking about a rollover — a rollout allows you to get the money out of taxable accounts in a way that minimizes unnecessary taxes and repositions your money into a tax-free financial vehicle like a properly structured, maximum-funded Indexed Universal Life policy (what we call an IUL LASER Fund).

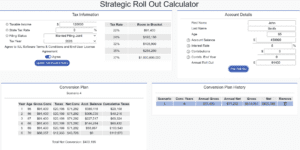

To illustrate what we mean, let’s look at a hypothetical example with a man we’ll call John Smith, a healthy 65-year-old with $120,000 in taxable income, with married filing joint status.

To illustrate what we mean, let’s look at a hypothetical example with a man we’ll call John Smith, a healthy 65-year-old with $120,000 in taxable income, with married filing joint status.

John just inherited a $450,000 retirement account that was growing at 6%, and he knows he doesn’t want to pay any more in taxes than necessary, so he comes to us for a strategic rollout.

We start by assessing his marginal tax bracket, which is 22% (using 2026 guidelines). With his current taxable income of $120,000, he has $91,400 of room left in his current tax bracket.

Now if he’s like many Americans with a good amount of savings set aside for retirement, he will likely not be in a lower marginal bracket in the next 10 years, so now’s the time to act.

To help him, we put together a rollout/conversion plan to withdraw $91,400 annually for Years 1 through 5, with the remaining $56,057 withdrawn in Year 6.

John will pay just over $20,000 in taxes the first five years (netting over $71,000), and a little over $12,300 in taxes (netting over $43,000) the last year.

Each year, he’ll put that withdrawn cash directly into an IUL LASER Fund. By the end of Year 6, he’ll have max-funded his IUL with just over $400,000 in premiums, and he’ll have the peace of mind of a death benefit of $650,000.

With his money tucked into an IUL, he’ll benefit from IUL’s unique advantages. It can now grow tax-free with predictable rates of return — IUL has historic average returns of 5% to 10% and is protected from market downturns with a 0% floor.

And he has the flexibility to use the money…or not. Should he want to access any of it, he can do so tax-free and penalty-free via policy loans.

And if he wants to leave it alone to pass the entire amount to his own heirs, he won’t be subject to a 10-year withdrawal period or RMDs. In other words, his death benefit (which typically blossoms as the years go on due to tax-free growth) can transfer to his loved ones completely income-tax-free.

Protect YOUR Inheritance

So if you have the good fortune of inheriting an IRA or traditional retirement account, we invite you to schedule a call with us.

We can run a strategic rollout analysis for you (like the one shown on this page), identify your marginal tax bracket status, and help you put together a plan to get any taxes over and done with as soon as possible.

From there, you can put that money to work in a tax-free environment, safe from market downturns, with predictable rates of return, and an income-tax-free transfer upon your passing.

Because as much as possible…it should be your inheritance, not Uncle Sam’s.

_____________________________