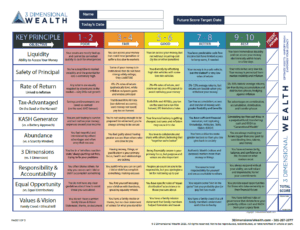

Hi, Doug Andrew here. In our, spring twenty twenty six edition of three-dimensional wealth living magazine, one of my favorite sections is on a tool. We have a spotlight on thirty nine different tools that empower you as a a a family leader. Okay? A parent or even a child or a business leader. And these tools will help you dramatically increase your productivity, your camaraderie, your compatibility, the harmony in your business or with your family, with your children, with your grandchildren. And so, in, the spring edition of three-dimensional wealth magazine, I’m the founder of three-dimensional wealth. One of my, favorite tools is featured in this one. It’s called raising your score And you start your journey, with this one tool and you’ll understand what I’m talking about. It’s found on pages twenty eight and twenty nine. The magazine has usually about forty pages. Okay? So it looks like this, raising your score. So, I have discovered in in my career that, when I, empower my students or my clients, my children, my grandchildren with a way to measure where they are at in every area or dimension of their life. Where are they at and then where are they wanting to go. Okay? Now, you may think that’s simple, but it’s amazing when, we teach concepts, and people learn a concept. They they don’t know where they’re at. They go, oh, okay. I got it. But they don’t ever take time. Well, where am I at and and where do I wanna go? What what is the delineation between, poor, fair, good, better and best. Okay? So this is why, I’ve created many many scorecards and the one that I’ve featured in in this edition is my favorite by far and this is because, whenever you’re gonna be going on a trip, let’s say, somewhere for the very first time, what’s the most important piece of information you need to know? You know, most people blurt out where you’re going or how to get there. No. A GPS uses triangulation. So it does that by honing in on three out of about thirty satellites that orbit this earth for that very purpose. Now, once it has clarity on where you are at within two square feet on this globe, Then you program in where you’re wanting to go and it’ll show you all kinds of ways to get to your desired destination. The freeway, the scenic way, the byway, where to refill your car or yourself in route. Okay? So that’s what a scorecard does. So, my scorecard that I developed years ago actually has fifty statements on it. Okay. There are ten overriding life changing principles that I have learned, in my I I’m just about seventy four years old. Okay. And these cover all three dimensions. So the the first four have directly to do with money. The the key elements of a prudent investment are liquidity, safety, rate of return and tax advantages. Okay? Now people learn about that, but then sometimes they they go, oh, my IRA four zero one k, is tax advantage. And that they don’t realize, no, that’s only fair. Tax deferred is only fair paying tax on the harvest when you get a bit of getting a tax break on the seed money, putting that pre tax dollars into an IRA or four zero one k is not the best way to go. In fact, it’s a far cry from the best way to go. It’s only a score of three or four. Okay? Now, Roths, I can prove, are are better than traditional IRAs or four zero one k’s if you, like most Americans, believe that taxes in the future will likely be higher. A Roth is better. Okay? But I put it here only in good. On a scale of one to ten, I would only give it a score of five or six out of ten. I would rather have the best. Okay? Which accumulates my money tax free. I can access that money tax free like a Roth, but I I have four additional advantages with my favorite vehicle, a property structure max funded indexed, IUL laser fund. I have four additional advantages that Roths will never have. Okay? So why would I mess around with a Roth? It has the two advantages of a Roth, it’s had it’s had those, for over a hundred and twenty years. Roths have only been around since nineteen ninety seven, but they have too many limits. You can only put in a certain dollar amount or certain percent of your income. You make too much money, you can’t even have a Roth. Did you know that? Okay. And so, I don’t like to mess around with inferior vehicles and unless you look at a scorecard, you would never know, unless you can rank it on a scale of one to ten. So this is where I invite clients in our educational webinars, on our live seminars to rate themselves on a scale of one to ten on the where the majority of their money is, where is it in regards to liquidity? The ability to access the money without triggering tax or a ten percent penalty or or having to sell the piece of real estate or whatever. Okay? Safety of principle to not lose when when the market goes down. I’m talking about the stock market or the real estate market. To earn a predictable rate of return that historically has outpaced inflation. Okay? And tax advantage is not just tax deferred, but totally tax free is the best. And so, whatever your score is, people fill it out over here when they would do the manual, sheet that I would give them. Okay? Well, these other six have to do with the other two dimensions. K a s h, the knowledge, attitude, skills and habits that you leave behind to your children and grandchildren instead of just a bunch of money. That will generate wealth into perpetuity instead of wealth running out, where if you just leave behind a lump sum of money to your children or grandchildren, it’s usually gone by the third generation and it ruins about half of them when they get just a lump sum of money. Okay? The difference between abundance mindsets and scarcity mindsets within a family or a business. A a three-dimensional approach instead of just one dimension. One dimension would be one leg of the stool just money, money, money instead of, the other two dimensions which are more important than the money. The these are the assets that that you truly cherish the most is not the money, it’s the wisdom, it’s the knowledge, it’s the family, it’s the relationship, it’s the values, it’s the experiences, okay? And then, being responsible and accountable, k. What we call dealing above the line instead of dealing below the line in the zone of blaming or justifying or operating in shame, which a lot of, families have children and, many companies have employees that deal below the line all the time. K. Equal opportunity instead of equal distribution. Instead of when you you pass away, all of a sudden chunk chunk chunk chunk, the the trust says it’s gonna be divided up equally and dumped in their laps. No. You you have, equal opportunity rules of governance, not equal distribution. Okay? So that if they have skin in the game and everybody has equal opportunities to have access to the money and the knowledge, attitude, skills, and habits, That’s equal opportunity instead of equal distribution. And then a values and vision statement where you can leave behind an ethical will because I I talk to people and ask them if they have a trust and then I say, yeah. I guarantee you, your kids and grandkids will never read that document except one page that says how much they get. Yeah. But I can capture a values and vision statement. They’ll they’ll read and reread, watch and rewatch, listen and re listen for generations, okay. So, once you understand these ten key principles of abundant living, you can score yourself on a scale of one to ten, and put it over here. Okay? And then add up your score. Now, it’s not where you begin with it really counts, but it it you have a score. Every everyone watching this has a score between one and a hundred and you score yourself. Now, I know the answer to this question. Whatever your score is today, how many of you know you would like to have a higher abundant living score in your future? Yeah. That’s what you want in the future. I would like a ten in all these. I I want a score of a hundred. But if you’re thirty two or forty three or sixty one, now you know where you’re at. And, then you can put down the score of where you want to be in six months or a year or whatever. And we’ve had many clients in less than a year take their score from from thirty two up to over ninety and oh my heavens, it it was incredible. So when you go into the article in the magazine, there will be a QR code, okay, in the article. And also if want, you can go to three-dimensional wealth dot com and if you go into that website, you click on learn more. Okay? And then click on the toolkit and then click on get the scorecard today. Now, there’s gonna be two versions there. One, you can download the PDF and just fill it out and have a hard copy or we just came out with a digital version. You click on digital and when you go through that scorecard here, you’ll just drag a a a little a little circle from here over until it it it’s where you’re at. Okay? So you don’t even have to fill out the number. It will auto fail based on how you dragged it over. So you could literally in in in three or four seconds say on liquidity, I’m here. On safety, I’m there. On rate of return, I’m there. You just drag the little circle over to where you’re at and it will it will populate and do the addition for you and you’ll have your score in less than less than a minute if you’re if you’re quick at this. Okay? So that’s what I wanna empower you with. Check it out, and, you will learn how to, grow your cash and cash in the magazine as well as, finding out where you’re at and where you’re wanting to go.

What’s with all the questions? As I often talk about, it’s important to regularly do GPS-style check-ins with ourselves, so we can see where we are today — and where we want to go tomorrow to elevate our lives.

What’s with all the questions? As I often talk about, it’s important to regularly do GPS-style check-ins with ourselves, so we can see where we are today — and where we want to go tomorrow to elevate our lives. That quest for clarity is why I developed the 3 Dimensional Wealth Scorecard. In about 15 minutes, this tool can give you a comprehensive snapshot of your progress in 10 aspects of Authentic Wealth.

That quest for clarity is why I developed the 3 Dimensional Wealth Scorecard. In about 15 minutes, this tool can give you a comprehensive snapshot of your progress in 10 aspects of Authentic Wealth.