The KASH Blueprint – Design an Architecture for Equal Opportunity

Establish a legacy of equal opportunity with your own KASH Blueprint

We all know that money can be the fuel that powers so many aspects of our lives.

Not only does it cover our basic necessities, like housing, clothing, and food, but it also makes life’s most worthwhile experiences possible. Education to expand our learning. Transportation to connect us with the people and places in our lives. Travel to increase our appreciation for the world around us. Charitable giving and humanitarian service to uplift those in need. And the list goes on and on.

The more abundance we can bring to our Financial Dimension, the more expansive our lives can be, right?

IUL’s Advantages

This is why so many savvy people turn to properly structured, maximum-funded Indexed Universal Life (what we call an IUL LASER Fund) — they know it can help them make the most of their money.

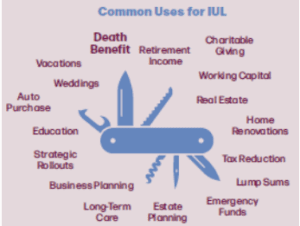

IUL’s liquidity provides access to tax-free income for everything from business ventures and retirement to education, travel, weddings, emergency funds, and more.

Its safety with a guaranteed 0% floor can protect your money from market downturns.

Its predictable rates of return (with historical average annual returns of 5% to 10%) can offer tax-free growth.

And IUL’s income-tax-free death benefit provides peace of mind, with a financial legacy that can be transferred on to your heirs.

Its versatility is why IUL is often called the Swiss Army Knife of financial vehicles.

But just having a Swiss Army Knife isn’t enough. It’s knowing how to use its many tools that makes a difference.

And one of the best ways to help your family know how to put your family’s financial resources to work? Create your KASH Blueprint.

Create a Plan for Using Your IUL

The KASH Blueprint can become your instructions for using the family’s Swiss Army Knife.

To illustrate, let’s say you have an IUL that you’ve established specifically for the family to access for living benefits. You’ve defined your family’s Values & Vision Statement, which includes things like

accountability, maintaining a strong work ethic, being abundance-minded versus entitlement-minded, etc.

And you’ve taken the step of completing your family’s KASH Blueprint, which outlines the rules of governance for how your family can access your 3 Dimensional Wealth assets. It’s based on principles of Equal Opportunity, rather than Equal Distribution. This means your children and grandchildren can’t just demand their equal share of money or support. Rather, that access is “earned” by adhering to your rules of governance.

Picture How It Works

To put this in real-world terms, let’s say you have three children, ages 16 to 25. Your 16-year-old wants to buy a car. You could just swoop in and pay for that car, which is lovely, but teaches her nothing about accountability.

Now let’s say part of your family’s Values & Vision Statement stresses taking ownership in life, and you’ve also completed your KASH Blueprint, which outlines how your children can request a “distribution or loan” from your family’s Legacy Bank for worthwhile endeavors.

So you set up a plan for her first car. You take out a policy loan, pay for the car with cash, and your teenager sticks to an agreed-upon repayment schedule over three years. You take her repayments, and put them right back into the IUL.

The advantages of this approach? IUL policy loans are tax-free and don’t come with the strict lending requirements you’d encounter with a bank or credit union.

And IUL policy loans don’t require repayment. If left unpaid, loan balances are simply deducted from the cash value/death benefit upon your passing.

So in a no-pressure environment, you can set up a plan for your 16-year-old to repay the policy loan over a reasonable amount of time. What’s more, this approach helps your teenager build financial muscles, confidence, and accountability.

Now let’s say your 19-year-old is in college, and her two-year scholarship is about to run out. She still has a couple years left in her undergrad program. Rather than shelling out the remaining tuition yourself, you can have her be accountable for a portion of her education.

You can take out a policy loan to pay for the tuition, and establish a repayment schedule for after she graduates. No bank, credit union, or Stafford loan red tape. No higher-interest student loans that can affect her credit rating down the road. Just a relaxed repayment schedule that reinforces accountability and integrity.

And let’s say your 25-year-old is a couple years into his career and is ready to buy a townhome. You could cover the down payment yourself, but you know it will help your son to get some skin in the game, so you take out a policy loan and set up a long-term repayment schedule that allows him to repay the loan, afford his new mortgage, and still have cash flow for his young adult life.

These rules of governance are already outlined in your KASH Blueprint, so there’s no debating, squabbling, or entitled demands for you to “just pay for everything!” Your children are growing in their ability to live within their means, make wise choices, and take accountability.

Design Your Own KASH Blueprint

With so many uses, IUL is the Swiss Army Knife of financial vehicles

Your KASH Blueprint can also cover rules for access to cash for things like business ventures, weddings, humanitarian giving, religious missions, emergency funds, and more. It also allows you to outline any rules of governance you might want to institute surrounding your family’s Intellectual and Foundational assets, as well.

By weaving accountability and responsibility into your children and grandchildren’s access to your family’s Legacy Bank assets, you set them up for independence and success, rather than dependency and entitlement.

Now keep in mind repayments might not always be in the form of money. You might outline that certain financial loans can be “repaid” with sweat equity, such as helping fix up the family cabin, or cleaning grandma’s home every week for a year.

Be prepared — at first, families who aren’t used to this kind of structure might feel like it’s a little “over-the-top” to create rules of governance, put them in writing, and enforce them.

But there’s nothing over-the-top about teaching your children the value of responsibility and accountability, about showing them how to fish, about giving them a hand up rather than a handout.

What’s more, by spelling everything out in your KASH Blueprint, you’re effectively helping your family avoid the infighting, jealousy, and destruction of relationships that too often arise over family wealth.

By giving everyone equal opportunity to access assets, there can be no in-fighting when Older Sister borrows money for a business venture and repays it on time. If Younger Brother someday needs money for his daughter’s wedding, then he has equal opportunity to borrow and repay the loan.

The guidelines are in place. Accountability is required. And family unity is preserved.

We invite you to download The KASH Blueprint and make it a part of your family’s 3 Dimensional Wealth.

Create your family’s 3 Dimensional Wealth rules of governance by downloading The KASH Blueprint today (available to all 3 Dimensional Wealth Community members). See how the Community can make a difference for your family by clicking here.